Indian banks migrating to digital channels; more on the evolution

The evolution of Indian banks migrating to digital channels can be traced back to the early 2000s when the Reserve Bank of India (RBI) started promoting the use of electronic payment systems. The introduction of the National Electronic Fund Transfer (NEFT) in 2005 and the Immediate Payment Service (IMPS) in 2010 were significant steps toward the digitization of payments.

However, the real push towards digital banking in India came with the demonetization drive in November 2016.

The sudden withdrawal of high-value currency notes led to a surge in digital payments, forcing banks to ramp up their digital infrastructure and services. Since then, there has been a significant increase in the adoption of digital channels by Indian banks.

Today, most banks in India offer a range of digital services, including mobile banking, internet banking and digital wallets.

Customers can access their accounts, transfer funds, pay bills and even apply for loans online or through mobile apps.

Banks also invest heavily in artificial intelligence, chatbots and other digital technologies to enhance customer experience and streamline operations.

The COVID-19 pandemic further accelerated the adoption of digital banking in India as customers increasingly relied on online channels to conduct their banking transactions.

Banks responded by launching new digital products and services, such as video KYC (Know Your Customer) and virtual credit cards.

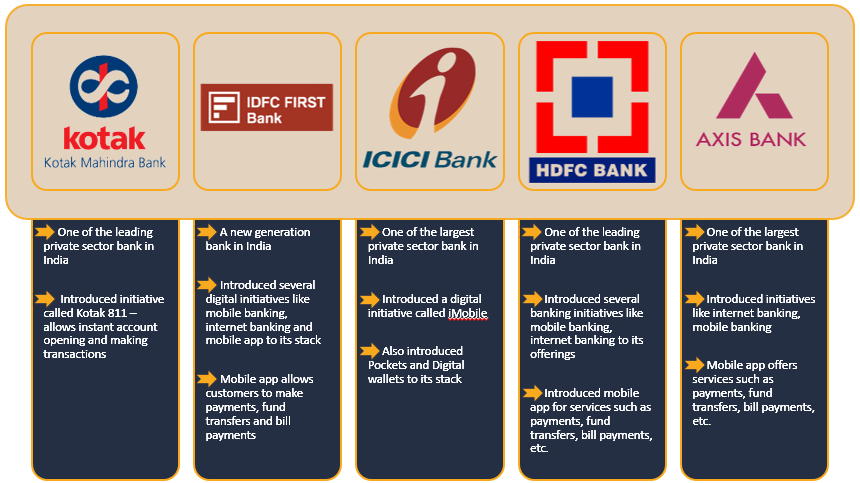

Examples of Banks that have revamped their offerings approach

Indian banks are increasingly adopting digital channels to provide a more convenient and efficient banking experience to their customers.

Whether it was Internet banking to reduce touchpoints or mobile banking to bring services to your fingertips, the transformation has been massive.

Building on the evolution, Indian banks also proactively introduced altering service designs and encouraged the use of contactless payments through technologies like the NFC, QR codes, mobile wallets, etc.

Today, urban India experiences the provision to make payments to street vendors too through digital methods.

It is a vision to convert India into a digital-first country from a cash-heavy economy and joining force with the banks to achieve the said vision is Fintechs.

Collaborating with Fintechs has accelerated the entire process whether in terms of internal operations of the bank or external aspects.

The evolution of Indian banks migrating to digital channels has been rapid and transformative and the trend is expected to continue as more customers shift towards digital banking.